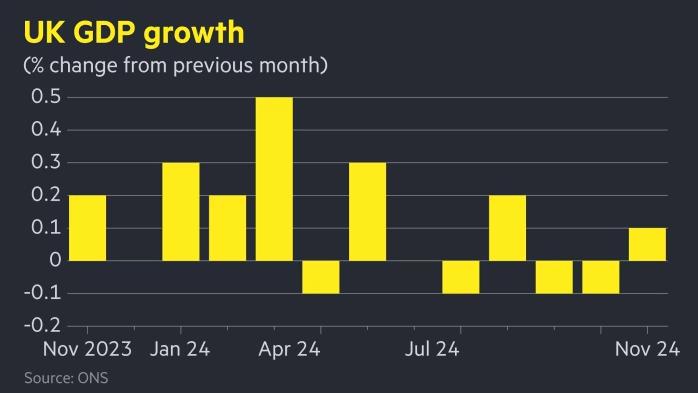

The UK economy grew for the first time in three months in November 2024, although growth fell far short of market expectations, further fuelling concerns about the economic outlook. The latest GDP figures, released by the Office for National Statistics (ONS), show that gross domestic product (GDP) grew by 0.1% in November after two consecutive months of contraction. The increase was mainly driven by bars and restaurants, as well as construction, but the increase was significantly below market expectations of 0.2 per cent.

First, according to the Statistics Office, real GDP did not grow in the three months ending in November 2024 compared to the three months ending in August 2024. Specifically, the services sector did not grow in the three months, while the manufacturing sector contracted by 0.3%. Nevertheless, the construction sector stood out, growing by 0.2%. The release of the data will no doubt deepen concerns about the long-term performance of the UK economy.

Second, the weak performance of the British economy has further amplified fears of stagflation, in which prices remain high even as economic growth falters. Stagflationary pressures prompted the central bank to raise borrowing costs sharply at the start of the year, but as expectations of a rate cut have grown, speculation about the future direction of boe policy has intensified. Growth in November, though weak, rebounded from previous months, with a 0.1% rise in the services sector in particular helping to offset a contraction in manufacturing. The result lifted the economy slightly, but it still shrank by 0.1% compared with March last year. Against the backdrop of constant policy adjustments by the Bank of England, investors' focus has shifted to the prospect of rate cuts in the coming months.

At the same time, according to market forecasts, the Bank of England is likely to start cutting interest rates in 2025, at least twice, by 25 basis points each. Nevertheless, some analysts believe that the size and timing of interest rate cuts are still uncertain, especially in the case of inflation data that is not as expected, the process of interest rate cuts may become more complicated.

Moreover, on the inflation front, the latest data for December showed that the annual UK inflation rate unexpectedly fell to 2.5% from 2.6% in November, which provided some positive signals for the market. The easing of inflationary pressures has led to sharp swings in government bond markets. Investors' expectations have shifted and they have increased their bets on future interest rate cuts from the Bank of England, sending yields on UK government bonds sharply lower. In particular, yields on 10-year and two-year government bonds fell 0.05 percentage points and 0.07 percentage points, respectively, reflecting heightened expectations of slowing economic growth and monetary easing in the UK. This reaction in the bond market further reinforces the market consensus for a rate cut, while investors generally believe that the central bank is likely to cut rates again by 25 basis points in February 2024.

Although November's data showed an uptick, the longer-term economic outlook remains grim. In its December 2024 forecast, the boe mentioned that the UK economy would show zero growth in the final quarter, a sharp downgrade from its previous forecast of 0.3% growth. Allen Taylor, an external member of the MPC, warned that the latest forward-looking indicators of activity pointed to a dimmer outlook for 2025 and called on the Bank of England to be more aggressive in cutting interest rates to address the economic challenges ahead.

In addition, some experts pointed out that although the British economy has a weak rebound in the short term, the overall economic growth rate is still weak, and the risk of long-term stagnation is greater. There was a recession at the end of 2023, followed by a rebound in early 2024, but there is widespread concern that the UK economy could slip back into stagnation.

Finally, in addition to slowing economic growth, the UK government's fiscal policy is also facing a large challenge. The Chancellor announced in his October 2024 budget that employers' national insurance contributions would be increased from April, a policy that could have a negative impact on the Labour market and the wider economy. Experts say the move could further drag on economic growth by raising labor costs and discouraging businesses from hiring and investment. Simon Pittaway, senior economist at the Resolution Foundation think tank, said the UK economy was performing like a "rollercoaster", with a short-term rebound not necessarily able to reverse the long-term slowdown in growth. Although the current economic data show some signs of recovery, in the longer term, the UK economy is likely to enter a state of stagnation, and further policy adjustments and stimulus measures will be necessary.

To sum up, although the UK economy recorded a weak growth of 0.1% in November 2024, this growth was far from the market's expectations, and was accompanied by a slowdown in the growth of the service sector and a contraction in the manufacturing sector. Despite rising interest rate cut expectations and cautious market expectations for future economic growth, the future of the UK economy still faces many uncertainties. In the longer term, the risk of economic stagnation remains, and the government and central bank may need to take additional policy measures to boost the economy, ease stagflation pressures, and lay the foundation for future growth.

According to Dawn News, recently, Chief Minister Syed Murad Ali Shah of Sindh Province has taken a series of measures regarding the wheat market.

According to Dawn News, recently, Chief Minister Syed Murad…

On July 1st local time, 404 Media, a foreign media outlet, …

From reaching a historical peak of $5598 per ounce in late …

On July 5, 2026, Yahoo Finance reported that QTS, a data ce…

In the early hours of July 6, the Russian military launched…

A survey conducted by the UK Financial Conduct Authority (F…

© Copyright 2026, All Rights Reserved