The concept of the "Trump Trade" has gradually taken shape in the financial markets since Donald Trump was elected President of the United States. During his election campaign and after his election, Trump put forward a series of economic policy proposals, which greatly influenced the expectations of market participants. From large-scale tax cut plans to financial deregulation, and then to large-scale infrastructure construction proposals, each policy implies far-reaching impacts on the U.S. economy and financial markets.

His tax cut plan mainly targets enterprises and high-income individuals, aiming to reduce the tax burden on enterprises and thus increase their profit margins. This expectation has made the market confident in the future cash flow and profit growth of enterprises. For listed companies, an increase in profits usually means higher dividend distributions and an increase in stock value, which directly stimulates the rise of the stock market. In terms of financial deregulation, the Trump administration intended to reduce the constraints on financial institutions, making their operations more flexible and enhancing their business expansion capabilities, which had a positive impact on the stocks of the financial sector. The large-scale infrastructure construction plan can not only directly stimulate the demand of related industries such as construction and raw materials, creating a large number of job opportunities, but also drive the development of the entire economy through the conduction of the industrial chain, further enhancing the market's expectation of corporate profitability.

Driven by the Trump Trade, the U.S. stock market has shown a trend of sector rotation and upward movement. The financial sector has performed strongly. Banks and other financial institutions have benefited from the expectation of rising interest rates, because a rise in interest rates will expand the net interest margin and improve the profitability of banks. At the same time, financial deregulation has enabled financial institutions to have more autonomy in risk management, business innovation and other aspects. For example, some large banks can more freely carry out investment banking business and capital market-related businesses, and their fee income and trading income are expected to increase, and their stock prices have also risen accordingly.

The industrial sector has also been positively affected. The infrastructure construction plan requires a large amount of industrial products such as mechanical equipment, steel, and cement. The orders of related enterprises have increased, their production scales have expanded, and the expected profit growth is obvious. For engineering machinery giants like Caterpillar, the demand for their products is closely related to infrastructure construction. Under the stimulation of Trump's policies, the market's expectation of their product sales and performance has been greatly increased, and their stock prices have continued to rise.

The technology sector has also performed outstandingly in this round of upward movement. On the one hand, the tax cut policy is conducive to technology enterprises increasing their R&D investment and profit retention. On the other hand, although there have been some frictions in Trump's trade policies, to a certain extent, they have also prompted technology enterprises to strengthen their competitiveness and innovation capabilities and seek new markets and development opportunities. Moreover, the overall upward atmosphere of the stock market has also attracted more funds to flow into technology stocks, pushing up their stock prices.

From the perspective of investor behavior, the Trump Trade has triggered optimistic sentiment among domestic and foreign investors towards the U.S. stock market. International investors regard the U.S. stock market as an important place for hedging and value appreciation, and a large amount of funds have flowed in. Whether it is sovereign wealth funds, pension funds or other institutional investors, they have all increased their allocations of U.S. stock assets. For domestic investors in the United States, the rise of the stock market has brought about a wealth effect, further stimulating consumption and investment.

The flow of funds has also shown diversified characteristics. In addition to the inflow of funds from traditional institutional investors such as mutual funds and pension funds, new investment entities such as quantitative investment funds have also adjusted their strategies according to market trends and increased their investments in sectors that benefit from Trump's policies. Moreover, in a low-interest-rate environment, investors who originally held fixed-income assets such as bonds have also begun to partially shift to the stock market in search of higher returns.

The yields of U.S. Treasury bonds have shown an upward trend under the background of the Trump Trade. On the one hand, the market expects that Trump's fiscal policies will increase the scale of government debt. In order to attract investors to purchase more Treasury bonds, the yields of Treasury bonds need to be increased. On the other hand, the expectation of economic recovery has increased, and the expectation of inflation has also risen. According to the Fisher effect, the nominal interest rate is equal to the sum of the real interest rate and the expected inflation rate. When the expectation of inflation rises, the yields of Treasury bonds will also increase accordingly.

The rise in the yields of Treasury bonds has a wide range of impacts on the entire financial market. For the bond market, the prices of old bonds fall and the issuance costs of new bonds rise. For the stock market, although there may be some adjustment pressure in the short term due to the rise in the cost of funds, in the long term, the expectation of economic improvement reflected by the rise in the yields of Treasury bonds has a supporting effect on the stock market. Moreover, the changes in the yields of Treasury bonds will also affect the foreign exchange market, and the U.S. dollar exchange rate may strengthen due to the rise in the yields of Treasury bonds, further affecting the exports of the United States and the profitability of multinational enterprises.

Similar changes have also occurred in the yields of corporate bonds. On the one hand, the environment of rising market interest rates has made the issuance interest rates of corporate bonds increase. On the other hand, the impact of Trump's policies on corporate profitability is uncertain, and the credit risk assessment is also changing. For enterprises with high credit quality, the yields of their bonds may be more affected by the rise in market interest rates; while for some enterprises that are highly dependent on Trump's policies and have relatively high risks, the yields of their bonds may rise by a larger margin due to the increase in credit risk premiums.

The changes in the yields of corporate bonds affect the financing costs and capital structures of enterprises. If the yields rise too quickly, the financing costs of enterprises will increase, which may affect their investment plans and expansion strategies, especially for those enterprises that rely on debt financing. However, for some enterprises with abundant cash flow and strong profitability, they may take advantage of the opportunity of the rise in the yields of corporate bonds to adjust their debt structures and reduce their financing costs.

Although Trump put forward a series of attractive economic policies, he faced many political and social resistances during the implementation process. For example, the tax cut plan needs to be approved by Congress, and there are serious differences among different political factions regarding the scale and targets of tax cuts. The source of funds for the infrastructure construction plan is also a problem. There are disputes over the limit of government debt ceiling and how to promote projects without overburdening the fiscal situation. If these policies cannot be implemented smoothly, the market expectations will be broken, and the stock market and yields may experience significant fluctuations.

The trade protectionist policies of the Trump administration have triggered trade frictions on a global scale. The United States has imposed tariffs on imported goods, and other countries have also taken corresponding retaliatory measures. This has had an impact on the international supply chains and export markets of U.S. enterprises. The costs of some enterprises that rely on imported raw materials have risen, while export-oriented enterprises are facing the risk of reduced orders. Trade frictions may also lead to a slowdown in global economic growth, which will have a negative impact on the U.S. stock market and yields, offsetting the original positive expectations of the Trump Trade.

The global economic situation is complex and changeable. The Trump Trade is formed on the basis of the expectations of U.S. domestic policies, but changes in the international economic environment may weaken its effects. For example, economic fluctuations in emerging economies, uncertainties in the European economy, and the coordination of global monetary policies may all affect the U.S. financial market. If there are signs of a global economic recession, the upward trends of the U.S. stock market and yields may not be sustainable and may even reverse.

The Trump Trade has had a significant impact on the rise of the U.S. stock market and yields, involving multiple levels of economic and financial fields from policy expectations to market reactions. However, this process is accompanied by many risks and uncertainties. The difficulties in policy implementation, trade frictions, and changes in the global economic situation may all change the current market trends. Investors and market participants need to closely monitor the changes of these factors in order to make reasonable decisions in the complex market environment, and policy makers also need to balance domestic and international economic relations while promoting domestic economic development to ensure the stability of the economic and financial markets.

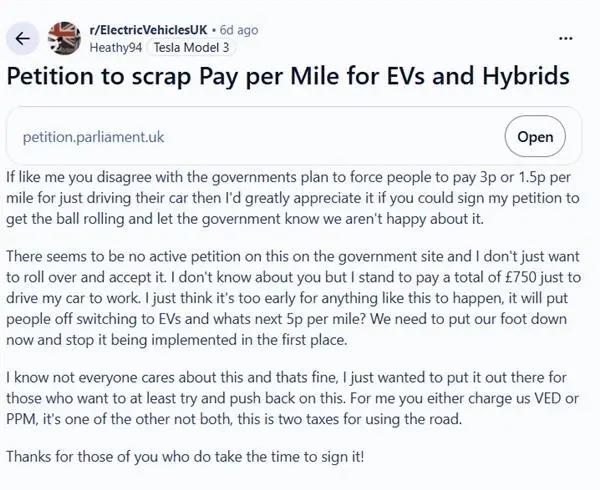

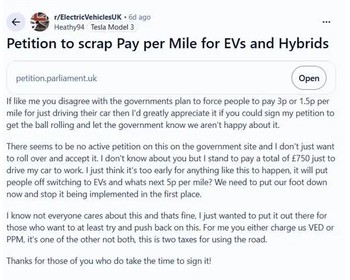

Recently, the British government has confirmed that a new vehicle consumption tax (eVED) system will be implemented on April 1, 2028, imposing a tax of approximately 17 yuan per 100 kilometers for pure electric and hydrogen-powered vehicles, while reducing the tax for plug-in hybrid models by half.

Recently, the British government has confirmed that a new v…

Under the dual pressures of war and sanctions, Iran is endu…

AP, Dubai — Military confrontation between the United State…

Recently, Reuters reported that Apple is accelerating its e…

In July 2026, the entire country of Japan was hit by a disa…

Recently, global convenience store giant 7-Eleven made head…

© Copyright 2026, All Rights Reserved