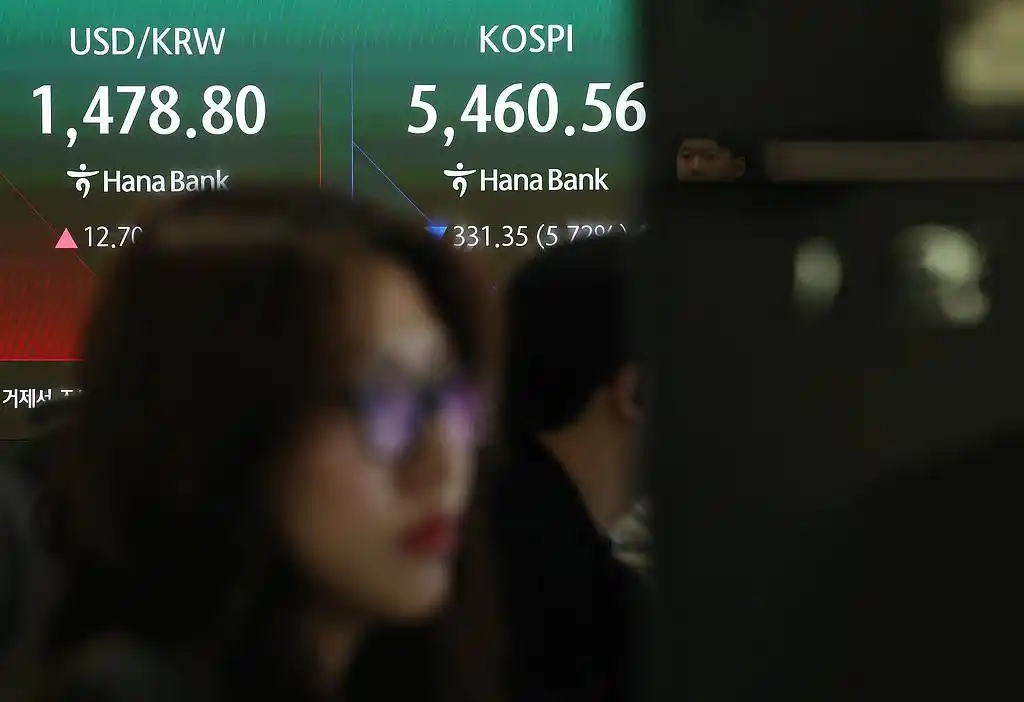

On March 3rd local time, the Korean stock market witnessed a historic slump, triggering the circuit breaker mechanism repeatedly. The Korean Composite Stock Price Index (KOSPI) closed down by 7.24%, marking the largest single-day decline since August 2024. During the overnight trading session on the 3rd, the exchange rate of the South Korean won against the US dollar dropped below the 1500 mark, reaching a low of 1506 won, which was the first time since the global financial crisis in 2009. The next day (March 4th), the decline further intensified, with the KOSPI index closing down by 12.06% at 5093.54 points, marking the largest single-day decline in history. The exchange rate of the South Korean won against the US dollar broke through the 1500 mark, reaching a new low in 17 years. This financial storm triggered by the Middle East geopolitical conflicts and exacerbated by its own structural vulnerabilities not only severely damaged the local financial system in South Korea but also had a profound impact on the global financial sector through capital flows, sentiment transmission, and industrial chain linkage, serving as a test for the resilience of global capital markets.

For the local financial market in South Korea, this slump triggered a chain reaction of "stock and currency double blow", exposing the fragility of the system. The proportion of foreign capital in the Korean stock market exceeded 30%, with high leverage among retail investors, and the proportion of margin trading reached 35%, with retail investors accounting for as high as 78%. This market structure magnified the impact of the slump sharply. The concentrated liquidation-style selling by foreign capital and the stop-loss orders of programmed trading formed a vicious cycle, causing market liquidity to be temporarily tight. A large number of retail investors faced the risk of margin calls, residents' wealth shrank rapidly, consumption willingness further declined, and it exacerbated the already severe household debt pressure in South Korea. At the same time, the depreciation of the South Korean won triggered the risk of imported inflation, and the rise in international oil prices pushed up the cost of imports in South Korea, further compressing corporate profits. Although the South Korean central bank urgently launched a 100 trillion won market stabilization plan, it was difficult to reverse the market panic in the short term.

The impact of the Korean stock market slump spread rapidly, triggering emotional resonance and capital reallocation in global financial markets. The Asia-Pacific markets were the first to be affected, with the Nikkei 225 index of Japan falling sharply, marking the largest decline since 2026, and foreign capital withdrew from emerging markets in the Asia-Pacific region, leading to regional liquidity tightening. As a core part of the global semiconductor industry chain, Samsung Electronics and SK Hynix of South Korea saw their stock prices plummet, directly dragging down the global technology stock trend. Nasdaq futures in the US market plunged before the opening, and leading companies such as NVIDIA and TSMC also turned green. Additionally, global funds began to shift from risky assets to safe-haven assets such as the US dollar and gold, and hedge funds urgently increased their positions in panic index futures to hedge risks, reshaping global investors' expectations for risky assets.

At the industrial chain finance level, the impact of the Korean stock market slump continued to spread along the global supply chain. South Korea's semiconductor exports accounted for one quarter of total exports, and Samsung and SK Hynix dominated the global storage chip market. Their stock price slump led to a downward shift in the valuation of enterprises, an increase in refinancing costs, and possible delays in expansion plans for production capacity, thereby affecting the global chip supply pattern. At the same time, South Korea's high-energy-consuming industries such as automobiles and petrochemicals were impacted by rising energy prices, with production costs rising, and their export competitiveness declined, potentially triggering price fluctuations and order adjustments in related global industries, and weakening South Korea's price competitiveness of its export products in the international market, further exacerbating the uncertainty of the global supply chain.

This Korean stock market slump further highlighted the interconnection and fragility of global financial markets. It warns that in highly interconnected global capital markets, local geopolitical risks may rapidly evolve into global shocks through capital, trade, and other channels. For emerging markets, excessive reliance on foreign capital, a single industrial structure, and excessive leverage can make them vulnerable in the face of external shocks. In the future, South Korea needs to address risks by optimizing its industrial structure, reducing its reliance on foreign energy, and improving the stability mechanism of the market. Meanwhile, global investors also need to reassess the investment risks in emerging markets and strengthen the bottom line for risk control. This financial shock is not merely a crisis but also a profound test of the resilience and risk prevention capabilities of the global financial system.

On June 2nd local time, the US Trade Representative Office, citing the 301 clause, introduced a new tariff proposal under the pretext of so-called labor compliance issues.

On June 2nd local time, the US Trade Representative Office,…

AP, Washington — The U.S. government has rolled out a new r…

According to a report by Reuters on June 2nd, the US Depart…

According to recent reports by US media, US President Trump…

Donald Trump is embroiled in the biggest corruption controv…

Recently, Trump has launched two core economic and trade me…

© Copyright 2026, All Rights Reserved