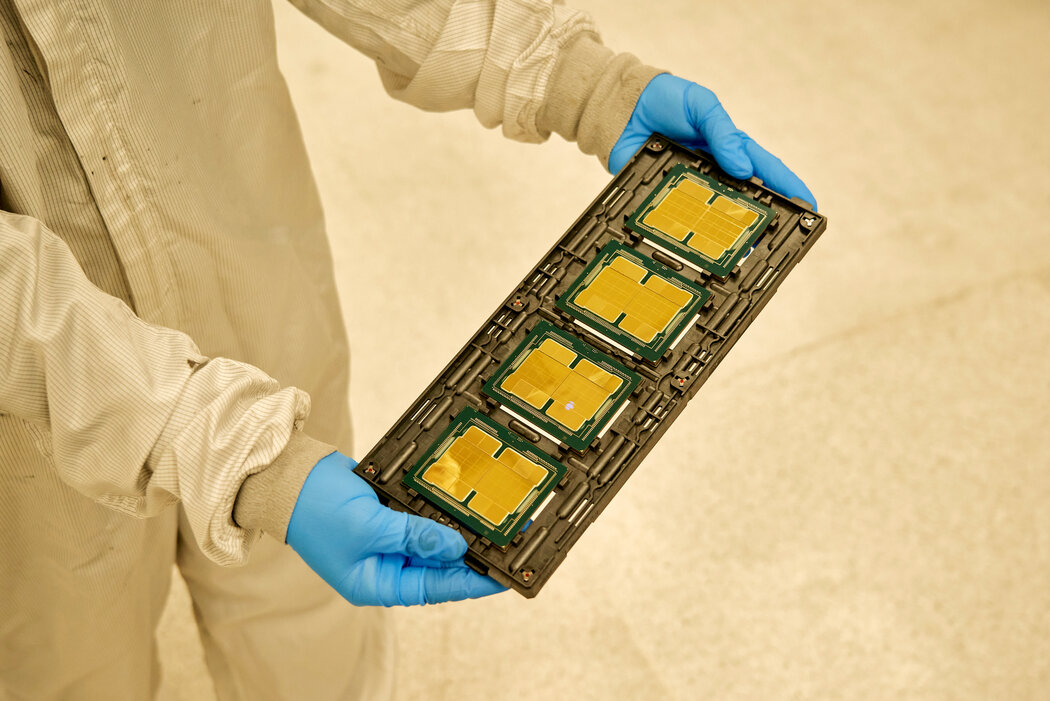

Recently, the United States plans to further expand the scope of AI chip export control to the global level, requiring companies such as NVIDIA and AMD to obtain permission from the US Department of Commerce for the export of high-end AI accelerator products. In some scenarios, even mandatory binding with US companies is required. Additionally, international chip manufacturers like Infineon and Texas Instruments have raised the prices of global analog chips since April 1st. This has led to a rapid intensification of the computing power competition dominated by geopolitics, which not only profoundly changes the business logic of the global technology industry but also pushes the electronic industry chain into a new stage of high costs and pattern reshaping.

This time, the United States has upgraded the AI chip control from targeted restrictions to global coverage. Essentially, it is using technological hegemony to interfere with the global market order and attempting to firmly grasp the dominant position in global computing power allocation. The previous precise containment targeting a single country has now transformed into a tough measure of using domestic laws to constrain the global industrial chain. High-end computing power chips are no longer purely commercial goods but have become strategic tools in geopolitical games. For American technology companies like NVIDIA and AMD, the global approval mechanism directly compresses their overseas market space. A large number of orders face the risks of delayed approval and termination of cooperation. The revenue growth logic of the enterprises is forced to be restructured, and the capital market also experiences continuous fluctuations. For AI enterprises and computing power service providers worldwide, they are forced to confront supply uncertainty. Enterprises that rely on US high-end chips for model training and computing infrastructure construction not only have to bear high hardware costs but also face complex compliance reviews. The risks and costs of business operations simultaneously increase.

Meanwhile, the global price increase of analog chips has further exacerbated the pressure on the entire industry chain. As core fundamental components in fields such as automotive electronics, industrial manufacturing, and consumer electronics, the price hikes of analog chips will gradually pass on the cost pressure from the upstream chip manufacturing to the downstream end products, and the entire industry is faced with the choice of either reducing profits or raising prices at the terminal level. The limitation of AI computing capacity construction and the increase in the cost of basic chips form a double squeeze, resulting in a slowdown in the global infrastructure construction of computing power. Small and medium-sized enterprises gradually exit the AI field due to their inability to bear the high costs, and industry resources are acceleratingly concentrated in the hands of leading enterprises. The competitive landscape of the global technology industry is increasingly showing a two-pole division trend.

Facing the technological control and price shock from the United States, the Asian chip manufacturing industry has accelerated the process of localization, becoming an important force to break the single-pole monopoly. Japan has increased its investment in advanced process chips and jointly formed an independent chip ecosystem with international forces; South Korea has relied on the advantages of storage chips and focused on the research and development of high-end HBM chips, strengthening its position in the AI server industry chain. Each country has realized the of over-reliance on a single supply chain, and has increased investment in technological research and industrial support, promoting the autonomy and controllability of chip design, manufacturing, packaging, and testing, in an attempt to occupy a position in the global computing power competition.

From a business perspective, although the global AI chip control by the United States consolidates its technological advantages in the short term, it has also completely stimulated the autonomous substitution willingness of the global industry chain. The development model of long-term reliance on American chips is unsustainable, and diversification of supply chains and technological autonomy have become the inevitable choice for various technology enterprises. The deep involvement of geopolitics in business has broken the development laws of market-led industries, bringing many challenges such as supply shortages, cost increases, and cooperation disruptions in the short term. However, in the long run, it will also promote the global technology industry chain to shift from single-pole dependence to multi-polar coexistence, and give rise to a more resilient and balanced industrial new pattern. For global enterprises, only by actively adjusting supply chain layouts, increasing investment in core technology research and development, and proactively responding to cost fluctuations, can they grasp the initiative in this fierce computing power competition.

Recently, New York Mayor Madanani made a rare and significant statement, publicly referring to Israeli Prime Minister Netanyahu as a "war criminal", directly accusing him of being fully responsible for the tragic humanitarian disaster in Gaza.

Recently, New York Mayor Madanani made a rare and significa…

The latest July survey data released by the ZEW – Leibniz C…

The Trump administration announced on Tuesday that it would…

On July 21st local time, Canadian Prime Minister Mark Carne…

According to the Associated Press, the latest data from the…

In mid July 2026, the situation in the Middle East will onc…

© Copyright 2026, All Rights Reserved